The Other K-Shape

The AI money circle is real. It's also sending a fortune straight into the pockets of companies most people aren't watching closely enough.

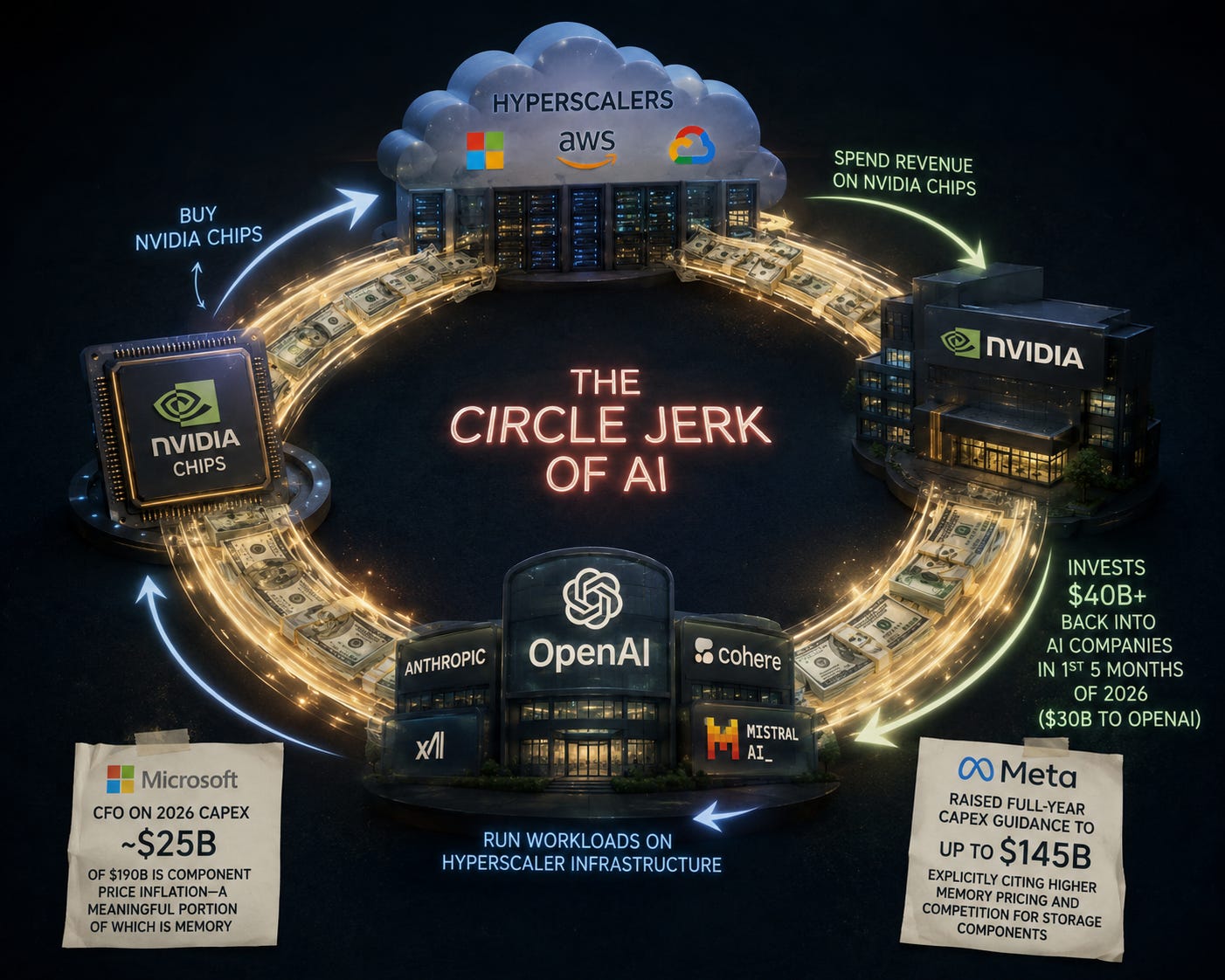

There’s a criticism of the AI trade that’s been floating around long enough to feel like crude wisdom: that it’s a “circle jerk.” That the same dollars are just orbiting each other in an increasingly expensive loop — hyperscalers buying Nvidia chips, Nvidia taking that money and investing $40 billion back into AI companies in just the first five months of 2026 (including $30 billion into OpenAI alone), those AI companies running their workloads on hyperscaler infrastructure, the hyperscalers spending that revenue on more Nvidia chips. Microsoft’s CFO, on the most recent earnings call, cited roughly $25 billion of its $190 billion 2026 capex as component price inflation — a meaningfully large portion of which is memory. Meta raised its full-year capex guidance to as high as $145 billion, explicitly citing higher memory pricingand competition for storage components.

The circle jerk critique is not entirely wrong. There is a circularity here. Nvidia invests in companies that buy Nvidia GPUs, which generates revenue for Nvidia, which it uses to invest in more companies that buy more GPUs. TechCrunch noted that the pattern across its public equity investments is consistent: capital flows to companies that buy Nvidia hardware at scale and re-rent it to hyperscalers and model builders. The industry has a word for this structure now: neocloud.

But here’s what the “it’s all circular” crowd gets wrong, or at least incomplete: money circling doesn’t mean it stays in the same pockets forever. As it flows, it leaks. And where it leaks — what it has to purchase along the way, what physical constraints it runs into, what bottlenecks it cannot bypass no matter how clever the software — that’s where the durable investment opportunity actually sits.

The hyperscalers and Nvidia are the center of the circle. But the circle cannot turn without memory. Without storage. Without the physical layer that every single AI workload (training, inference, agentic, whatever comes next) runs through on its way to actually doing something. And the companies providing that physical layer are, right now, experiencing the most favorable supply-demand environment of their existence. They’re still being priced, in large part, like the party ends any quarter now.

That’s the K-shape I want to talk about. Not the income inequality version — the Morgan Stanley “haves vs. have-nots” consumer spending piece, which is real and well-documented and exactly as investable as a congressional hearing. The one happening inside the stock market, where a group of companies is riding an arm that goes up, and another group is riding an arm that goes down, and the market hasn’t finished pricing either of them correctly.

Part I: The Circle, Described Honestly

Google, Amazon, Microsoft, and Meta collectively plan to spend $725 billion on capital expenditures in 2026 — up 77% from last year’s record $410 billion. Add Oracle’s $50 billion commitment and you’re over $700 billion from five companies. Capital intensity at Microsoft has hit 45% of revenue. At Oracle it’s 57%. Amazon is projected to go negative on free cash flow this year by as much as $28 billion, according to Bank of America analysts. Meta’s free cash flow is expected to drop almost 90%. These companies are not being conservative about this buildout.

Now. What does $700+ billion in capital expenditure actually buy?

Data centers. GPUs and CPUs. High-bandwidth networking. Power infrastructure. And, increasingly the binding constraint in the whole system, memory and storage. Microsoft staying capacity-constrained through 2026 despite $190 billion in spending is not a GPU problem at this point. It is a memory and power problem. The GPU can sit in the rack. If it doesn’t have the memory bandwidth to feed it, it sits there doing nothing particularly interesting.

This is the leak in the circle. And the companies the leak flows through — Micron, SanDisk, Western Digital, Seagate — are the ones I keep coming back to.

Part II: The Upper Arm — What the Earnings Are Actually Saying

The conventional AI trade is Nvidia at a $3+ trillion market cap and 35-40x forward earnings. I understand why people own it. The story is real. But the discovery premium is gone: every institutional fund on earth has already made that bet, and the multiple expansion story from here requires near-flawless execution on a timeline that is, charitably, uncertain.

What is not fully priced (and what the earnings reports of the last two quarters have been screaming at anyone paying attention) is the memory and storage layer. Let me put the numbers from today’s close on the table, because they say more than most analysis does.

Micron (MU) — $795.33 today (+6.5%), 52-week range $90.93–$818.67

The 52-week range alone is worth sitting with for a moment. A year ago this stock was trading below $100. It closed today at $795. That is not a small-cap story. That is the largest memory company in America rerating in real time as the market slowly internalized what the earnings were saying.

Micron’s fiscal Q2 2026: revenue of $23.86 billion, up from $8.05 billion in the same quarter a year prior. Net income of $13.79 billion, or $12.07 per share, versus $1.58 billion and $1.41 per share a year ago. Operating cash flow of $11.90 billion. In ninety days. Net profit margin sitting at 41.47%, gross margin at 58.44%, operating margin at 48.34%. Return on invested capital at 31.63%. These are not the metrics of a commodity business in a cyclical boom. These are the metrics of a company that has stumbled into genuine pricing power.

The valuation numbers are what stop me cold every time I look at them. Price/Earnings TTM: 35.26x, which sounds fine. But Price/Forecasted Earnings (forward): 13.84x. PEG ratio on 5-year projected growth: 0.22. CFRA rates it Above Average. LSEG consensus is Buy. EPS growth forecast for the next year: 593%. EPS growth forecast over 3–5 years: 159.76%.

The market is still applying a cyclical commodity discount to a company that has sold out its entire 2026 HBM supply under multi-year contracts, with clients now signing three-to-five year supply agreements rather than the quarterly negotiations that used to define this industry. CEO Sanjay Mehrotra has been consistent: “As AI evolves, we expect compute architectures to become more memory-intensive.” That’s not promotional language. That’s a description of how the underlying technology works. More capable models need exponentially more memory. There is no architectural reason to expect that to reverse.

Micron estimates the HBM total addressable market growing from $35 billion to over $100 billion by 2028 — while simultaneously acknowledging it can only supply half to two-thirds of what customers are currently asking for. The company cannot keep up with demand. D.A. Davidson initiated coverage with a Buy and a $1,000 price target, calling it an AI-driven memory supercycle. The stock is at $795 today (up 70%+ year-to-date) and is, by any growth-adjusted valuation metric I know how to apply, still cheap.

SanDisk (SNDK) — $1,547.56 today, 52-week range $35.79–$1,600.00

If Micron is the story the market is slowly understanding, SanDisk is the story the market is currently in the middle of repricing at a pace that leaves most analysts looking like they’re reporting on a completely different company than the one in the earnings release.

SanDisk became an independent public company on February 21, 2025, when Western Digital completed the spinoff of its Flash business. It started life as a standalone stock around $34. It closed today at $1,547. It is the top-performing stock in the entire S&P 500 year-to-date in 2026, up roughly 429%, having already run approximately 350% in 2025 before that.

The most recent quarter: revenue of $5.95 billion, up 97% year-over-year, against analyst estimates of $4.70 billion. Adjusted EPS of $23.41 against a $14.54 estimate. Q4 guidance of $7.75–$8.25 billion versus analyst consensus of $6.49 billion. The analysts are consistently a full quarter behind the business.

Current fundamentals from today’s data: net profit margin 34.26%, gross margin 56.04%, return on assets 30.08%, return on equity 39.38%, return on invested capital 33.78%. Forward EPS growth forecast: 2,060%. EPS growth year-over-year TTM: 400.97%. Current ratio 4.78. Zero long-term debt. CFRA: Strong Buy. LSEG consensus: Buy.

SanDisk locked in NAND supply by renewing its manufacturing joint venture with Kioxia through 2034 — supply and cost certainty through the mid-2030s, at a moment when wafer capacity is the single biggest constraint in the industry. That’s not a software moat. That’s a physical moat, signed into contracts, running for the next eight years.

The forward P/E of 23.96x on a business with over 2,000% forward EPS growth and no debt is a number that I genuinely struggle to explain as anything other than the market still treating this as a spinoff novelty rather than a standalone AI infrastructure powerhouse.

Seagate (STX) — $834.01 today (+6.56%), 52-week range $100.00–$841.31

Another 52-week range that deserves a moment of quiet reflection. One hundred dollars to $841. In twelve months.

The HDD market has consolidated to three players globally: Western Digital, Seagate, and a distant Toshiba. Bank of America has called it an oligopoly outright. And in an oligopolistic market sitting at the intersection of “every AI workload generates persistent data that has to live somewhere” and “supply is fully allocated through calendar 2026,” you get the kind of pricing dynamics that the HDD industry hasn’t seen in its entire existence.

Seagate’s most recent quarter: free cash flow of $607 million, up 305% year-over-year. Management describing nearline capacity as fully allocated. Morgan Stanley raising its price target from $558 to $767. Morningstar revising fair value up roughly 50% and stating flatly: “We now believe the fundamentals around Seagate have structurally changed.” Seagate is already shipping 36-terabyte drives on its Mozaic 3+ HAMR platform, with 36-44 TB drives in the pipeline — technology that makes the previous generation of HDD economics look like a different industry.

Current data: net profit margin 21.60%, gross margin 41.57%, return on invested capital 44.02%. Sales growth 1-year: 28.92%. EPS growth TTM: 53.82%. EPS growth forecast 1-year: 83.63%. EPS growth forecast 3–5 years: 67%. Bull-case from Bank of America’s analyst: earnings nearly doubling to $45 per share by 2028, price target $700.

The trailing P/E of 74.22x looks high. The forward P/E of 56.07x still looks high. But on a 67% projected 3-5 year EPS growth rate, and with a business that management, Morgan Stanley, and Morningstar have all independently described as having structurally changed, the question is whether you’re paying 56x for a cyclical or 56x for a durable compounding machine that the market hasn’t yet agreed to treat as one.

Western Digital (WDC) — $515.83 today (+7.46%), 52-week range $46.40–$525.15

The same story, the pure-play HDD version. WDC completed the separation of SanDisk on February 21, 2025, and is now a focused hard drive business — which turned out to be excellent timing, because what it shed (flash, in SanDisk) went on to become the best-performing stock in the S&P 500, and what it kept (HDD) became one of the best-performing sectors in the market.

WDC Q3 FY2026: revenue of $3.34 billion, up 45% year-over-year. GAAP gross margin exceeding 50%. Free cash flow of $978 million in a single quarter. Q4 guidance implying 36-44% year-over-year growth. A 20% raise in the quarterly dividend. CEO Irving Tan on the call: “Virtually every AI workload, from training, inference, agentic AI to physical AI, creates data that is stored persistently and cost-efficiently on HDDs.”

Current fundamentals: net profit margin 55.03%, return on equity 85.63%, return on invested capital 60.03%. Sales growth 1-year: 32.04%. EPS growth TTM: 452.99%. EPS growth forecast 1-year: 104.32%. Zero long-term debt. Current ratio 1.49.

The forward P/E of 51.21x and the price/cash flow of 84.41x are the numbers the bears point to. The PEG ratio of 0.51 on 5-year projected growth is what I point back to. Schwab has this as a “D” — 81st percentile ranking — which is its most cautious rating and, frankly, the most interesting divergence in the whole group given the underlying fundamentals. Analyst consensus across LSEG is Buy. Argus rates it Buy. CFRA rates it Above Average. The rating agencies that use forward-looking analysis are pointing one direction; the rating model that leans on historical price behavior is pointing the other.

Part III: What Unites These Four (And Why the Framing Matters)

The reason MU, SNDK, STX, and WDC belong in the same analytical frame is not that they’re all “tech.” It’s that they all occupy physical chokepoints in the AI buildout that no software solution can substitute. You cannot run a frontier model without Micron’s memory. You cannot store the inference output without Seagate’s drives. Microsoft has $80 billion in Azure orders it literally cannot fulfill due to power and component constraints. The bottleneck is physical. The companies sitting at it are pricing accordingly.

This is also what distinguishes them from Nvidia as an investment thesis at this point. Nvidia faces at least a theoretical risk that efficiency breakthroughs reduce per-workload GPU requirements. Memory and storage demand scales with data, not with compute efficiency: smarter models generate more context, more outputs, more data that has to be stored somewhere. The direction of demand is not ambiguous. And unlike the software businesses I’m about to describe, none of these companies’ competitive positions are being eroded by the thing they’re profiting from. AI is Micron’s customer. AI is Seagate’s customer. The circle flows through them, not around them.

Part IV: The Lower Arm — Pricing Power Erosion, With Receipts

Now the part of the K that goes in the other direction.

I want to be clear about what I’m actually arguing here, because “SaaS is dead” is not the argument. The argument is more specific and, I think, more useful: the economic model that justified the premium valuations assigned to a generation of enterprise software companies — predictable, high-margin, per-seat recurring revenue with net retention above 100% — is breaking in ways that the current valuations haven’t fully absorbed. The businesses may survive and some will thrive. The multiples predicated on the old model’s predictability are repricing, and that repricing is not finished.

The mechanism is what matters. A single AI agent can now replace dozens of software licenses formerly held by human employees — what the market started calling “seat compression.” The per-seat SaaS model grows when customers add headcount. It stagnates, and eventually compresses, when AI agents replace headcount rather than augmenting it. Research Affiliates documented this directly from Q4 2025 earnings calls: multiple SaaS vendors confirmed that customers were using AI capabilities as leverage to negotiate lower costs for the same number of seats.

IDC now projects that pure seat-based pricing will be obsolete for 70% of vendors by 2028. The companies adjusting fastest — Salesforce with “Agentic Work Units,” Workday with “Flex Credits,” ServiceNow with consumption-based “Assist Packs” — are pivoting the whole revenue model in real time. That’s impressive. But “successfully pivoted the pricing model under existential pressure” is a different investment story than “compounding, predictable, high-NRR recurring revenue machine.” The former warrants a lower multiple than the latter. ServiceNow fell approximately 28% in 2025 pricing that in. The repricing isn’t finished.

The second thing happening on the lower arm is the commoditization of intelligence itself. Stanford’s AI Index 2025 documented inference costs falling 280-fold in roughly two years — from $20 per million tokens in late 2022 to $0.07 in late 2024. Any company whose competitive moat rested on “proprietary AI capability” is now defending a moat that costs pennies per million tokens to replicate.

The Trade Desk collapsed from above $141 to approximately $37-38 by year-end 2025 — an ad-tech intermediary whose value proposition evaporated when AI could optimize the whole funnel end-to-end without paying the platform a cut. Intuit fell nearly 46% from peak as the workflows it charged to manage started getting done for free. Neither company “failed” in a business sense. Both got repriced because the pricing power that justified their premium multiples turned out to be time-limited.

Adrian Helfert at Westwood ran the numbers across 460 S&P 500 companies, scoring each on both moat strength and AI disruption risk. Companies most exposed to AI underperformed the most AI-resilient by nearly 26 percentage points in just the first seven weeks of 2026. The market is doing the sorting. It hasn’t finished.

The question for every tech position you own (and it’s the question I run through my own portfolio) is simple: does this company sit at a physical chokepoint that AI needs, or does it sit in the path of something AI is about to make cheaper or redundant? The former is the upper arm. The latter is the lower one. Both groups still share an ETF, a CNBC segment, and the generic label of “tech.”

They are not the same investment.

Conclusion: Follow the Leak

The “AI circle jerk” critique of the market is more right than wrong as a description of the center. Nvidia invests in companies that buy Nvidia chips. Hyperscalers fund AI labs that run on hyperscaler infrastructure. The center is self-referential and getting more so.

But the circle leaks. It has to. And what it leaks into — the memory that makes every GPU cluster actually function, the storage that holds every inference output, the physical infrastructure that turns $700 billion in hyperscaler capex into something that actually runs — that’s where the money flows that doesn’t flow back.

Micron at $795 with a 0.22 PEG, 593% forward EPS growth, sold-out 2026 HBM supply under multi-year contracts. SanDisk at $1,547 with zero debt, 2,060% forward EPS growth, NAND supply locked through 2034. Seagate at $834 with 67% projected 3-5 year EPS growth and nearline capacity fully allocated. Western Digital at $515 with 55% net margins, 60% ROIC, and a CEO who has articulated the demand thesis more cleanly than most analysts have.

These are not hidden stocks. They’ve moved. But the forward fundamentals still look disconnected from the cyclical-commodity framing the market keeps applying. The rating agencies using backward-looking models say “C” and “D.” The rating agencies using forward-looking analysis say “Buy” and “Strong Buy” across the board. At some point the earnings close that gap.

The circle keeps turning. The leak keeps flowing. I’d rather be sitting at the place it flows through.

The information and opinions expressed in this article are for educational and informational purposes only and do not constitute financial, investment, or trading advice. Past performance is not indicative of future results. While every effort has been made to ensure accuracy, the data and projections presented are based on publicly available information as of the date of publication and are subject to change without notice. Readers should conduct their own due diligence or consult a qualified financial advisor before making any investment decisions. The author holds no obligation to update or revise this content in light of new developments.